Thomas J. Smedinghoff

© 2021, IDPro, Thomas J. Smedinghoff

Table of Contents

The Identity System Legal Environment 2

The Legal Rules Governing Identity Systems 5

Level 2 – Generic Identity System Law 8

Level 3 – Individual Identity System Rules 9

Introduction

What are the legal rules that govern identity systems? What obligations do those rules impose on the participants involved?

The reality is that identity systems and their participants are governed by a myriad and complex set of laws, regulations, and contractual requirements, and the obligations they impose are not always clear. To make sense of it all, it is best to focus first on the legal environment that governs identity systems.

Terminology

-

Consumer Protection Law - laws and regulations that are designed to protect the rights of individual consumers and to stop unfair, deceptive, and fraudulent business practices.

-

Contract Law – laws that relate to making and enforcing agreements between or among separate parties.

-

Fraud Law – laws that protect against the intentional misrepresentation of information made by one person to another, with knowledge of its falsity and for the purpose of inducing the other person to act, and upon which the other person relies with resulting injury or damage.

-

Identity Theft Law – laws governing crimes in which the perpetrator gains access to sensitive personal information belonging to the victim (such as birth dates, passwords, email addresses, driver’s license numbers, social security numbers, financial records, etc.), and then uses this information to impersonate the victim for personal gain, such as to commit fraud, establish credit in the victim’s name, or access the victim’s accounts.

-

Privacy Law - laws that regulate the collection, use, storage, and transfer of personal data relating to identified or identifiable individuals.

-

Tort Law - the body of law that covers situations where one person’s behavior causes injury, suffering, unfair loss, or harm to another person, giving the injured person (or the person suffering damages) a right to bring a civil lawsuit for compensation from the person who caused the injury. Examples include battery, fraud, defamation, negligence, and strict liability.

The Identity System Legal Environment

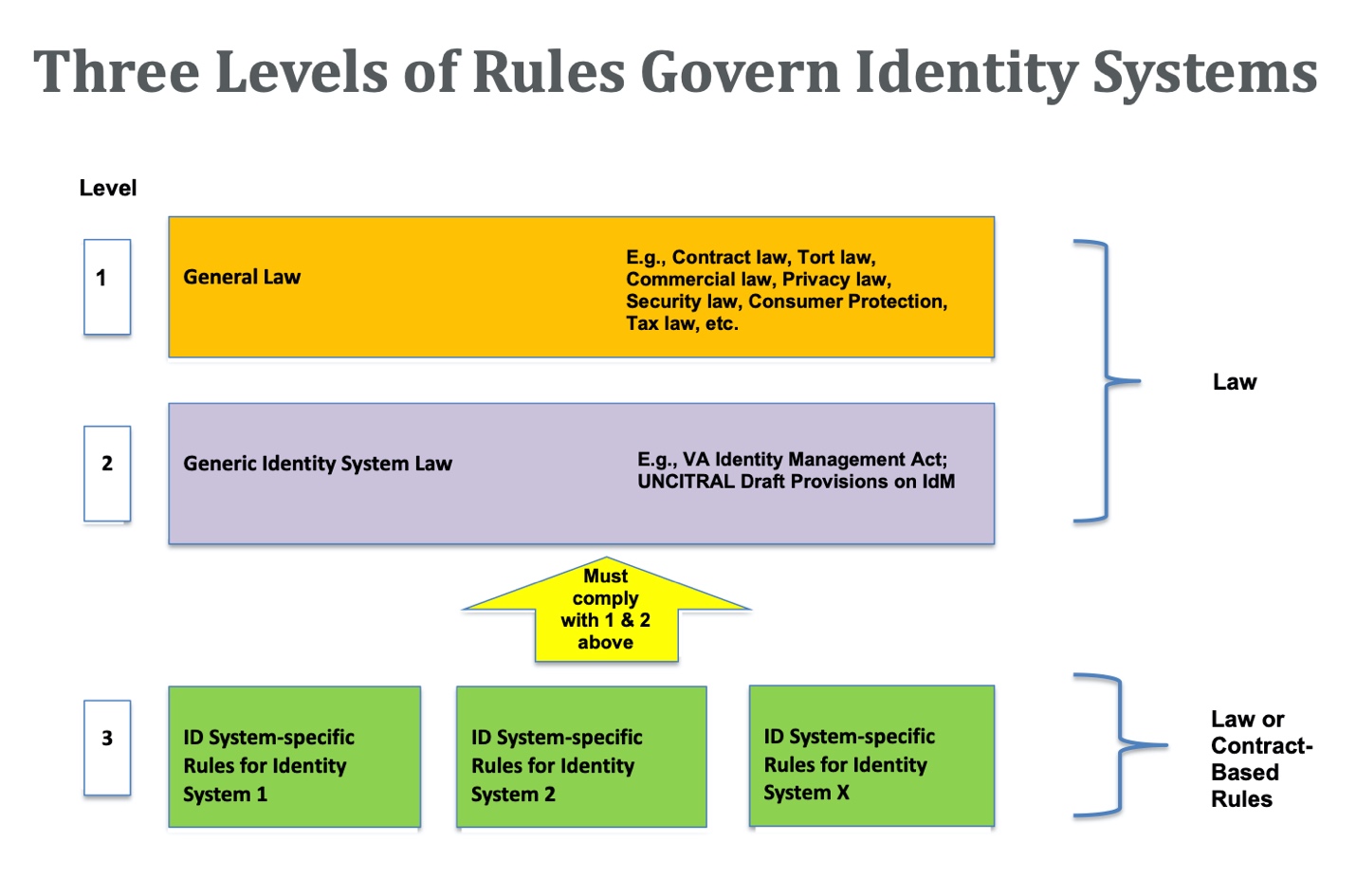

At a high level, the legal environment that governs the operation of any identity system consists of three different levels of legal rules, categorized as follows:

-

Level 1: General Law : The first level is law that applies generally to all business and personal activities. This law covers a wide variety of subjects and is not written with identity systems in mind, although it is frequently applied to identity system activities where appropriate. Examples of general law that might affect the operation of an identity system include contract law, tort law, privacy law, warranty law, and consumer protection law.

-

Level 2: Generic Identity System Law : The second level of legal rules consists of law written specifically to govern identity systems generally. Level 2 identity management laws typically apply to all identity systems within a jurisdiction and are often relatively high level in nature. At present, however, very few such Level 2 laws exist. Examples of such generic identity system law include Virginia’s Electronic Identity Management Act[1] and the Draft Provisions on the Cross-border Recognition of IdM and Trust Services[2] being developed by the UN Commission on International Trade Law (UNCITRAL). In many jurisdictions, Level 2 law for identity systems does not yet exist.

-

Level 3: Individual Identity System Rules : The third level of legal rules consists of the set of system-specific rules written to govern the operation of a particular identity system. These rules provide the technical, business, and operational specifications and rules for the identity system, specify the rights and responsibilities of the participants and govern the relationships between the various parties. They can be quite detailed but apply only within the confines of the identity system they were written to govern.

For private sector identity systems, these legal rules are typically contract-based, are often referred to as a trust framework or system rules, and apply only to those system participants who have contractually agreed to be bound to them. Examples include the SAFE Identity Trust Framework (previously the SAFE-BioPharma Trust Framework),[3] the Sovrin Governance Framework,[4] and the SecureKey Concierge Trust Framework.[5]

For government identity systems, these Level 3 legal rules are often embodied in a law or regulation enacted by the government and thus automatically apply to all those who participate in the identity system. Examples include the eIDAS Regulation in the European Union,[6] the Identity Documents Act in Estonia,[7] and the Aadhaar Act in India.[8] In some cases, however, government identity systems also use contract-based trust frameworks, such as the Trusted Digital Identity Framework (TDIF)[9] for the Australian national federated identity system.

The Level 3 portion of the legal environment for any identity system is under the control of the developers of that identity system (government or private sector). That is, the operators of a private sector identity system are free to make up the Level 3 system rules and design them in the manner best suited to meet the goals of that specific identity system. However, where such rules are contract-based, they will apply only to the participants that agree to be bound by them, and they may be supplemented (and in some cases overruled) by existing laws and regulations at Levels 1 or 2. In other words, the Level 3 rules designed for any specific identity system must comply with existing law – a challenge made all the more difficult for identity systems that cross jurisdictional boundaries.

The structure of this identity system legal environment

is summarized on the diagram below.

This structure of the identity system legal environment is very similar to that which governs a credit card system (such as Amex ® , Discover ® , MasterCard ® , or Visa ® ). Each credit card system is governed by Level 3 system rules developed by the operator of that system (e.g., the MasterCard Rules[10] and the Visa Core Rules and Visa Product and Service Rules[11]). Those rules provide the technical, business, and operational specifications for the specific credit card system and govern the relationships between the various parties. They are made binding on the parties that participate in the system (e.g., credit card holders, merchants, issuing banks, processors, etc.) by contract.

Those Level 3 credit card system rules and the associated contracts are also governed by: (1) Level 1 general law (e.g., the law of contracts, the law of negligence, etc.), and (2) Level 2 generic credit card system law written to regulate all credit card systems (e.g., Regulation Z[12] in the US). Like the legal environment governing identity systems, this combination of Level 3 system rules and contracts and Level 1 and 2 law forms the legal environment in which each credit card system operates.

The Legal Rules Governing Identity Systems

Level 1 – General Law

Currently, most law applicable to identity systems is general law (Level 1). Typically, this law was written for a purpose completely unrelated to identity management (e.g., tort law, contract law, warranty law, privacy law, etc.) and without considering how it might apply to identity systems. In fact, in many cases it was written before the concept of identity systems even existed. And in some cases, the law developed over hundreds of years via common law and court decisions. Nonetheless, such general law often applies to identity system-related activities, often in ways that were unanticipated at the time of its original adoption.

Identity systems primarily deal in information. Thus, the Level 1 law that applies to identity systems will typically include those laws that address various aspects of transactions involving information. This primarily includes law governing the following aspects of information:

-- Collection, Use, and Transfer of Identity Information

Identity information about individuals is personal data, and identity system processes typically involve the collection and processing (by an identity provider, attribute provider, or its agents) and disclosure (to a relying party) of such personal data about a subject. Thus, privacy laws will regulate the collection, storage, use, and transfer of identity information and will have a major impact on all identity system participants and all identity system transactions. This may include, for example, imposing limits on what data may be collected, requirements regarding notices of collection practices, limits on the use that may be made of such data, and restrictions on the transfer of such data to third parties and/or across country boundaries.

-- Accuracy of Identity Information

A key concern of all participants in an identity system relates to the accuracy and reliability of the identity information they are communicating or relying upon. Inaccurate identity data can cause a variety of problems for persons who rely on that data, as well as liability for those who provide it.

Laws governing providing false or incorrect information, whether intentionally or negligently, will be relevant in the evaluation of the rights, obligations, and liabilities of the participants in identity systems, including identity providers, attribute providers, and data subjects.

Key among them are fraud laws and identity theft laws. Fraud involves a representation of fact (or material omission of fact) that is intended to deceive another to their material detriment. Identity theft occurs when a party acquires, transfers, possesses, or uses someone’s personal information in an unauthorized manner, with the intent to commit, or in connection with, fraud or other crimes.

Even in the absence of fraud, the tort of negligent misrepresentation can create liability for communicating false information. This occurs where the information is intended for the guidance of others in their business transactions, but the information provider did not exercise reasonable care in determining the accuracy of the information prior to the communication. Thus, in certain circumstances, an incorrect assertion of one or more identity attributes might qualify as a negligent misrepresentation.

This tort of negligent misrepresentation creates a duty to exercise reasonable care or competence to verify facts and creates liability for incorrect representations made without exercising reasonable care about the accuracy of the facts asserted. However, it does not make the supplier of information (e.g., the identity provider) a guarantor of the accuracy of an identity assertion. Generally, the information provider does not have liability for inaccurate or “false” information unless the provider failed to exercise reasonable care in obtaining or communicating the information.

To the extent that incorrectly communicated identity information damages the reputation of the data subject, the tort of defamation may also be relevant. Defamation involves a false or disparaging statement of fact about a person that is published to a third party causing the person to suffer harm. It is possible that incorrect identity or attribute assertions could be considered defamatory in certain situations. For example, asserting an inaccurate attribute – e.g., age, medical information, sexual orientation, political affiliation, or employment -- might be considered defamatory in certain cases where the named person suffered harm as a result.

The accuracy or reliability of identity attribute information communicated to a relying party by an identity provider or attribute provider may also be governed by warranty law. A warranty is an assurance, promise, or guaranty by one party to another party that facts or conditions are true and may be relied upon by the other party.

A warranty may be either express or implied. An express warranty arises from specific statements made by one party to another. Such statements may be made in writing, such as in a contract or advertisement, or may be made orally, such as by a sales representative. For example, an identity provider’s published processes may include a warranty regarding the quality of the information it provides to relying parties.

An implied warranty is an unspoken, unwritten promise created by law that arises from the nature of the transaction and the inherent understanding by the recipient rather than from the express representations of the provider. Implied warranties are based upon the common law principle of “fair value for money spent.” Thus, for example, a court could conceivably conclude that identity providers make implied warranties regarding the reasonableness of the processes they used to collect and verify identity attribute data.

Finally, it is important to note that some privacy laws also regulate the accuracy of personal data. The EU GDPR, for example, requires that personal data maintained by data controllers (such as identity providers) must be “accurate and, where necessary, kept up to date” and that “every reasonable step must be taken to ensure that personal data that are inaccurate … are erased or rectified without delay.” Article 5(1)(d). In addition, it provides that “The data subject shall have the right to obtain from the controller without undue delay the rectification of inaccurate personal data concerning him or her.” Article 16.

-- Availability, Retention, and Deletion of Identity Information

In the case of identity systems where an identity provider, relying party, or other identity system participant retains data about a data subject, the availability, retention, and deletion of such identity information can be regulated by a variety of Level 1 laws.

Privacy law (e.g., GDPR and the California Consumer Privacy Act (CCPA)[13]) often regulates the availability of personal data (and hence identity data) to the data subject. In particular, such laws often impose on identity providers a duty to provide individual data subjects with access to the data it has collected about them, as well as information regarding the purposes for which it collects and processes such data, and the recipients or categories of recipients to whom the data are disclosed

Numerous laws also impose data retention obligations on companies regarding their corporate records. These laws may apply to and require both identity providers and relying parties to retain certain identity data for a particular period of time.

Finally, however, privacy laws (such as the GDPR) may impose limits on the retention of personal data. And increasingly, privacy laws (such as GDPR and CCPA) grant data subjects are right to request that data about them be deleted or erased.

-- Security of Identity Information and Processes

Many data security laws and regulations impose obligations on companies with respect to the security of personal data and other information in their possession or under their control. To the extent that a participant in an identity system is collecting, using, storing, or transferring personal data, such data security laws may have a significant impact on its obligations and potential liability. This is particularly true for identity providers and relying parties.

Data security laws are sometimes incorporated into privacy laws, but regardless of form, they generally impose two key obligations: (1) a duty to provide reasonable security for personal data, and (2) a duty to disclose breaches of security of personal data to the persons affected and to regulators. Although not written specifically to address identity system activities, such laws will undoubtedly apply to the personal data used by identity systems as well.

Level 2 – Generic Identity System Law

The application of existing general law to identity systems is often not a good fit, frequently ambiguous, and in many cases leads to arguably inappropriate results. This is further complicated by the fact that the Level 1 laws applied to identity systems can vary considerably across jurisdictions. Thus, there have been several attempts to address these concerns.

Some jurisdictions have proposed, and some have enacted, legislation or regulations expressly governing all identity systems within their jurisdiction. However, there is not yet agreement on the desirability or goals of such generic legislation, much less on how to achieve them. Key questions yet to be resolved include whether such legislation should be designed to: (1) simply remove legal barriers (actual and perceived) to identity systems, (2) encourage and assist the development of identity systems, or otherwise help establish the “trust” and the “predictability” needed by parties engaged in online identity transactions, or (3) regulate and control identity systems, such as by protecting the privacy of personal information, ensuring the security and trustworthiness of identity transactions, or imposing or limiting the liability of identity providers.

At present, very little Level 2 law exists. Nevertheless, some noteworthy efforts to develop Level 2 law governing identity systems include the following:

Virginia . The state of Virginia became the first US state to adopt Level 2 identity legislation by enacting the Virginia Electronic Identity Management Act in 2015. That legislation is focused primarily on the issue of liability. To do that, it provides for the creation of a Virginia Identity Management Standards Advisory Council, which was tasked with developing Identity Management Standards. Identity providers and trust framework operators that comply with the requirements of those Identity Management Standards are then granted immunity from civil liability. In other words, the Virginia Act provides a safe harbor from liability for identity providers and trust framework operators.

UN Commission on International Trade Law (UNCITRAL) . In the Spring of 2015, both the American Bar Association Identity Management Legal Task Force, and a group of EU countries (Austria, Belgium, France, Italy, and Poland, with support from the EU Commission), submitted proposals to UN Commission on International Trade Law (UNCITRAL) regarding identity management legislation. Those proposals recommended that UNCITRAL undertake a project to develop “a basic legal framework covering identity management transactions, including appropriate provisions designed to facilitate international cross-border interoperability.” UNCITRAL has since agreed to move forward with such a project.[14]

UNCITRAL provides an international forum capable of developing a harmonized set of globally accepted law governing identity management. Such law can be adapted domestically by individual countries to promote a universal approach to identity management law and can be extended globally (to facilitate cross-border identity transactions) through an international treaty or convention.

In September 2019, UNCITRAL produced the second version of its Draft Provisions on the Cross-border Recognition of IdM and Trust Services. Issues currently being considered include the:

-

Rights and responsibilities of various identity system roles

-

Determination of the reliability of identity systems

-

Liability of identity providers

-

Legal recognition of identity credentials.

-

Cross-border recognition of identity credentials.

Level 3 – Individual Identity System Rules

Both Level 1 and Level 2 law provides general rules applicable to all identity systems. But because each identity system is unique, it also requires its own tailored set of more detailed rules to govern its operations.

In fact, having predictable and enforceable rules designed to ensure that it functions properly and is trustworthy is key to any identity system. Unique system rules (e.g., a trust framework) will ideally provide such a structure to govern the operation of an identity system, much like the Visa or MasterCard rules rules (including the payment card industry data security standard or PCI-DCSS) that govern credit card systems.[15] Such rules include the technical specifications and operational rules and requirements necessary to make the system functional and trustworthy and the legal rules that define the rights and legal obligations of the parties and facilitate enforcement where necessary.

These individual identity system rules are the Level 3 law that governs an identity system. For private sector identity systems, these rules typically take the form of a so-called trust framework and are made enforceable against the various system participants by contract. Accordingly, those rules must comply with any restrictions at Levels 1 and 2 law.

In the case of public sector identity systems (such as a national ID system), these rules usually take the form of legislation or regulations adopted by the government to govern the system. Many countries, including most notably Estonia and India, have adopted laws to govern their specific national ID systems. In some cases, a country may establish an identity system based on a set of rules that participants voluntarily agreed to by contract. The Australian Trusted Digital Identity Framework (TDIF), and the UK GOV. UK Verify program takes this approach.

Regardless of whether an identity system is public or private, the issues addressed by the Level 3 system rules/trust framework often include the following:

-

technical specifications that will govern the system

-

rights and obligations of participants in each system role

-

data subject registration and enrollment processes

-

identity verification process requirements

-

credential issuance requirements

-

authentication process requirements

-

rules governing reliance by relying parties

-

data security requirements (over and above requirements of applicable law)

-

privacy requirements (over and above requirements of applicable law)

-

audits, assessments, and certification requirements

-

allocation of liability risk among roles

-

termination rights and obligations

-

dispute resolution

-

enforcement of rights and obligations

Where such rules are embodied in laws or regulations issued by a government, they are of course binding on all system participants by force of law. But in the case of a trust framework (typically used in a private-sector system), the system rules are binding on the participants only to the extent they agree by contract to be bound to comply with the rules. In all cases, however, the Level 3 law is comprised of system rules written for a specific identity system, and thus its applicability is limited to that system.

Author Bio

Thomas J. Smedinghoff is Of Counsel at Locke Lord, LLP, and Chair of the American Bar Association Identity Management Legal Task Force. He can be reached at Tom.Smedinghoff@lockelord.com

Change Log

| Date | Change |

|---|---|

| 2021-06-30 | Editorial updates |

[1] Code of Virginia - Chapter 50. Electronic Identity Management Act. 2015. https://law.lis.virginia.gov/vacode/title59.1/chapter50/ .

[2] “Draft Provisions on the Cross-border Recognition of IdM and Trust Services,” revision A/CN.9/WG.IV/WP.160, United Nations Commission on International Trade Law, last revised 16 September 2019, https://uncitral.un.org/sites/uncitral.un.org/files/media-documents/uncitral/en/wp-160-e.pdf .

[3] “Greater Security via the SAFE Identity Trust Framework,” accessed 18 May 2021, SAFE Identity, https://makeidentitysafe.com/trust-framework/ .

[4] “Sovrin Governance Framework,” accessed 18 May 2021, Sovrin, https://sovrin.org/library/sovrin-governance-framework/ .

[5] “SecureKey Concierge Trust Framework,” accessed October 10, 2019, SecureKey, https://securekey.com/resources/trust-framework-securekey-concierge-in-canada/ .

[6] eIDAS Regulation[EU]: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=uriserv:OJ.L_.2014.257.01.0073.01.ENG

[7] Identity Documents Act [Estonia]: http://www.unhcr.org/refworld/docid/4728ab1b2.html

[8] Aadhaar Act https://uidai.gov.in/images/targeted_delivery_of_financial_and_other_subsidies_benefits_and_services_13072016.pdf .

[9] “Trusted Digital Identity Framework,” accessed 18 May 2021, Australian Government Digital Transformation Agency, https://www.dta.gov.au/our-projects/digital-identity/trusted-digital-identity-framework .

[10] “Mastercard Rules,” accessed 18 May 2021, Mastercard, https://www.mastercard.us/en-us/about-mastercard/what-we-do/rules.html .

[11] “Visa Core Rules and Visa Product and Service Rules,” 15 October 2013, accessed 18 May 2021, Visa, https://usa.visa.com/dam/VCOM/download/merchants/visa-international-operating-regulations-main.pdf .

[12] “§ 1026.1 Authority, purpose, coverage, organization, enforcement, and liability,” 12 CFR Prt 1026 (Regulation Z), Consumer Financial Protection Bureau, accessed 18 May 2021 https://www.consumerfinance.gov/rules-policy/regulations/1026/ .

[13] “California Consumer Privacy Act of 2018,” Title 1.81.5, Section 1798.100, Part 4 of Division 3, State of California, accessed 18 May 2021, https://leginfo.legislature.ca.gov/faces/codes _displayText.xhtml?division=3.&part=4.&lawCode=CIV&title=1.81.5.

[14] UNCITRAL, “Colloquium on Identity Management and Trust Services,” 21-22 April 2016, accessed 18 May 2021, https://uncitral.un.org/en/colloquia/electronic_commerce/2016 .

[15] PCI Security Standards Council, Standards Overview, website, https://www.pcisecuritystandards.org/standards/.